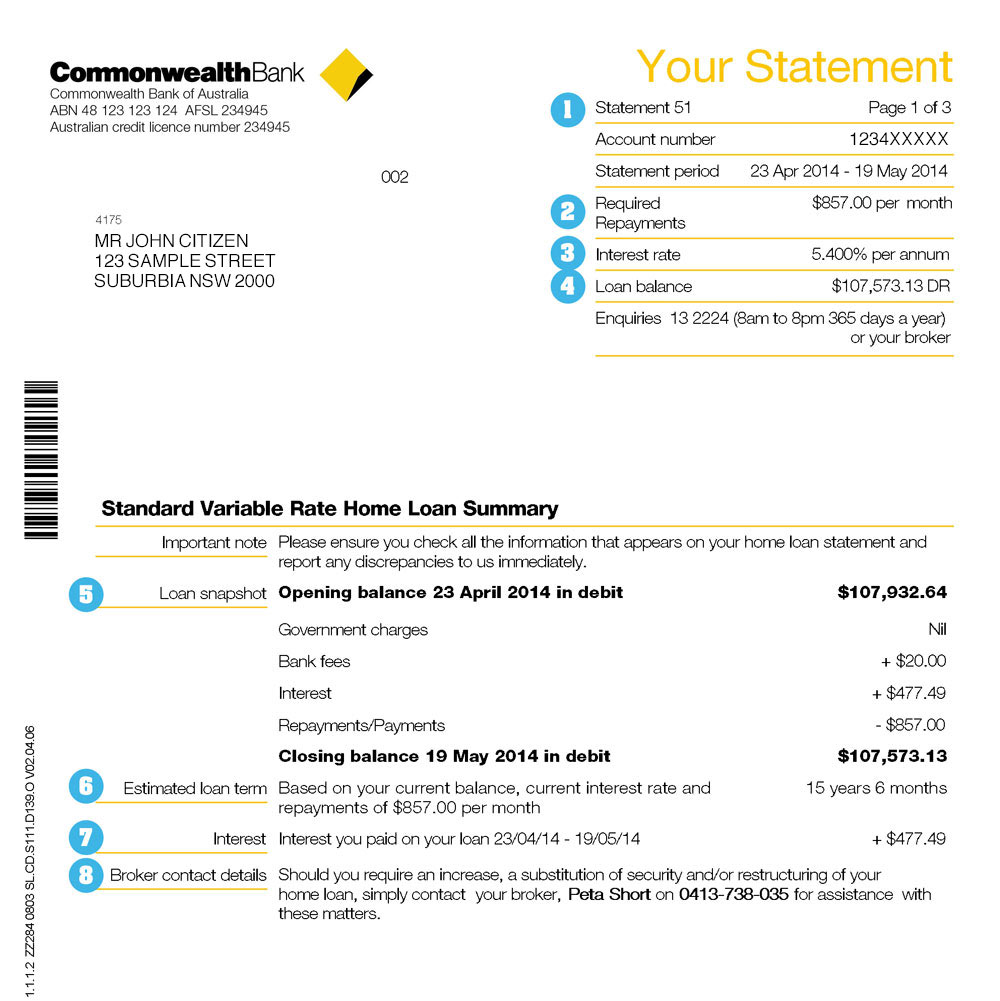

Mortgage Amortization with Even more Principal Payments Having fun with Excel

Throughout the amazing amortization plan example We left out a component which is of interest to many some one: adding a lot more dominant payments to pay back the loan prior to when the loan contract needs. Within course we shall create this particular aspect.

In advance of we get come allow me to discuss one important thing: You can typically (actually in so far as i understand it is obviously) just go full ahead and increase the amount of currency into be sure you send out on the home loan upkeep business. They will often shoot for you to definitely subscribe and purchase a course which enables you to definitely spend a lot more prominent, but this isn’t called for. Their application commonly immediately use any extra total the remaining dominant. I’ve done so for years, additionally the mortgage statement always suggests the extra principal percentage actually even if I’ve over nothing more than spend extra there is no need to have another look at or the mortgage organizations approval. Actually, I’ve refinanced my personal mortgage several times over the years and you can all of the mortgage servicer did so it. Dont inquire further, proceed and discover what happens.

If you have not yet , read the prior example, I will suggest which you do it now. We’ll use the same first style and you can wide variety right here. Definitely, there may have to be specific change, and we will add some new features. not, the basic tip is similar apart from we can no longer explore Excel’s based-from inside the IPmt and you can PPmt services.

Creating brand new Worksheet

Note that we have all of your own recommendations that we you would like on upper-kept place of the spreadsheet. You will find a good \$200,000 financial to possess 30 years with monthly obligations at a six.75% Apr. During the B6 We have determined the standard homeloan payment using the PMT setting:

Of course, We have adjusted the pace and you may amount of costs to a monthly base. Remember that We have inserted the fresh new costs a year for the B5. This is simply in case you ortize a thing that enjoys other than monthly payments.

Mortgage Amortization which have Most Dominating Costs Having fun with Prosper

You will also see that I’ve inserted the other principal and is paid off into B7. I’ve set it up to \$300 four weeks, you could alter you to definitely. Observe that within example I suppose you will make an equivalent a lot more percentage every month, and that it can start for the earliest fee.

Just like the we simply cannot make use of the built-inside the qualities, we will see to accomplish the brand new mathematics. Fortunately, its rather very first. The attention commission should always feel determined basic, and it is basically the for each months https://www.paydayloanalabama.com/morrison-crossroads (right here monthly) interest rate moments the rest dominant:

Such as for example, whenever we have the fee number in the B13, following we can calculate the initial desire commission in the cell C13 as: \$B\$4/\$B\$5*F12, and very first dominant payment inside D14 given that: B13-C13.

It’s just not a little that simple, no matter if. As the we’re going to include a lot more costs, we need to ensure do not overpay the borrowed funds.

Prior to we are able to determine the eye and you can dominant we need to assess the fresh payment. It turns out that people don’t use the founded-from inside the PMT function going back fee whilst will be another type of matter. So, we should instead estimate one last payment based on the desire for the last day additionally the left dominant. This is going to make our very own payment formula a bit much harder. Inside B13 enter the algorithm:

Remember that on dominating inside D13, In addition extra a min mode. This is going to make sure that that you do not shell out more than the remaining prominent number. We currently content those people algorithms down seriously to line 372, that may help us has actually up to 360 money. You can stretch they next if you want a longer amortization period.