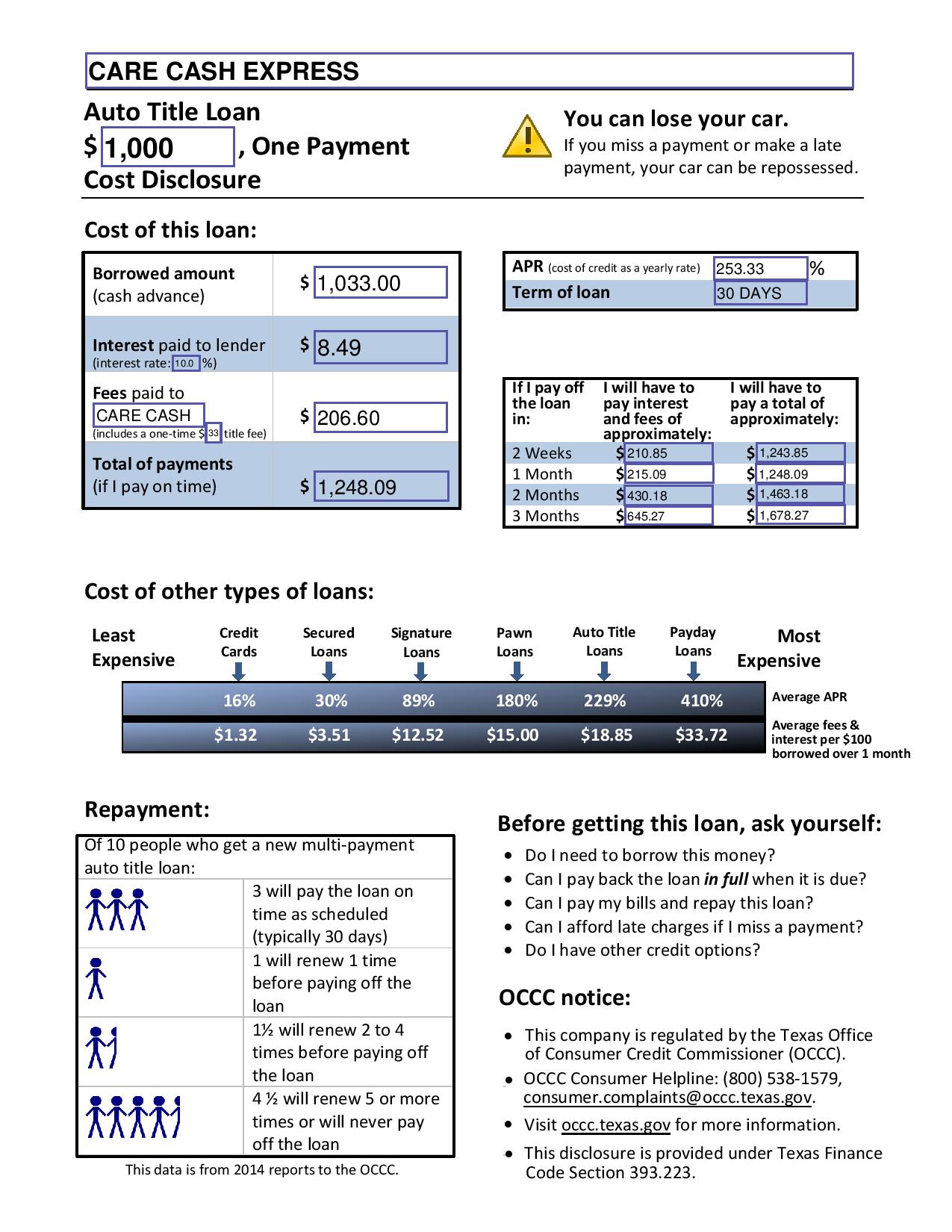

The primary delivery route regarding Speed / Hero money is by using do-it-yourself builders

Clients I have worked with have obtained sales demonstrations in their homes from the builders. One of many benefits associated with the pace / Champion program showed from the contractor’s sales force you’d be the brand new downright ability to without difficulty be eligible for the loan. Character loan qualifications don’t have any credit score specifications. Hence, property owners which have lower credit ratings, exactly who may well not qualify for almost every other funding possibilities, may be able to be eligible for a pace / Character mortgage. That yes be viewed as an advantage if not have the funds to cover residential solar panels or a special rooftop or other high efficiency home improvements.

Another advantage presented may be the taxation virtue. As with home loan funding, the capacity to itemize and deduct the attention (with your property taxes) in your tax returns would-be felt a large virtue, particularly for those people homeowners from inside the quite highest income tax mounts.

By the Rate loan’s attachment for the house’s property taxation, efficiently integrating the complete loan and its particular installment for the possessions income tax money, a speed mortgage seems glamorous versus other styles away from funding that have no newest influence on a beneficial homeowner’s taxes

Particular can even make a far-reaching comparison of one’s financial attract deduction compared to. the speed financing property taxation comparison (deduction). Some might conclude that not only ‘s the focus income tax-deductable, however, thus ‘s the prominent repayment too, that isn’t the fact which have a home loan. He or she is kept with only the closing documents and you will yearly property income tax bills as the ammunition having tax thinking.

Intuit, the application giant you to definitely deal the fresh new Turbo Taxation application, keeps this to express to the its site away from Champion mortgage tax deductions, Based on webpage 151 off Irs Book Zero. 17, the principal portion of the payment are allowable for repairs, however to possess developments. Towards many tactics, I am able to think it distinction bringing a small blurred on income tax big date. Tend to that it build individuals to possess a prospective Internal revenue service audit problem, otherwise will it act as a larger taxation advantage used by consumers and CPAs? The solution seems not sure and without instance history.

As opposed to a home loan business that always delivers a year-prevent Form 1098 mortgage attract reduced report to possess tax purposes, Champion financing individuals dont receive any comparable season-prevent report

In addition, the fresh new tax testing and costs assists a keen amortized fee plan one to pays off the lien during the discussed identity, thus a number of dominant protection is roofed in the annual comparison (payments). So it theory of using dominant repayments about income tax deduction will get getting a stretch in certain products not as opposed to precedent.

Whenever Mello Roos tests very first inserted the image more than two decades before, the genuine property community cautioned property owners from the subtracting the new Mello Roos portion of income tax payments on the tax returns. Folk You will find ever discovered did just take those people deductions, even though they was technically an incredibly quick portion of good thread fee. The individuals bond payments obviously tend to be prominent and amortize too. Officially, the latest homeowner gets a great deduction on dominating avoidance part of percentage, whereas that is not the situation having a home https://clickcashadvance.com/personal-loans-la/ loan percentage, where just the notice try tax deductable. I am not familiar with people negative consequences off declaring the individuals write-offs. Be told, we are not giving tax suggestions, so make sure you check with your income tax professional with this number.

An alternative advantage displayed by the builders is that duty otherwise evaluation stays to the possessions, it can also be commercially feel gone to live in this new holder. (But not, there may be certain significant problems with which assumption!) This time of one’s funding elizabeth on how much time it want having our home. When they uncertain on residing in our home for a lengthy period to recuperate its financing regarding the project, which possible work with would be tipping area you to facilitates brand new sale, particularly having residential solar panels which can be so popular.